Procedures for constructing a CI

Suppose \(X_1, X_2, \cdots, X_n\) are i.i.d. normal, with unknown mean \(\theta\) and a known variance1 \(\sigma^2\).

\[

\hat{\Theta}_n=\frac{X_1+X_2+\cdots+X_n}{n}

\]

\[

\hat{\Theta}_n \sim \text{N}\bigg(\theta, \frac{\sigma^2}{n}\bigg)\;\;\rightarrow\;\;\frac{\hat{\Theta}_n-\theta}{\sigma/\sqrt{n}} \sim \text{N}(0, 1)

\]

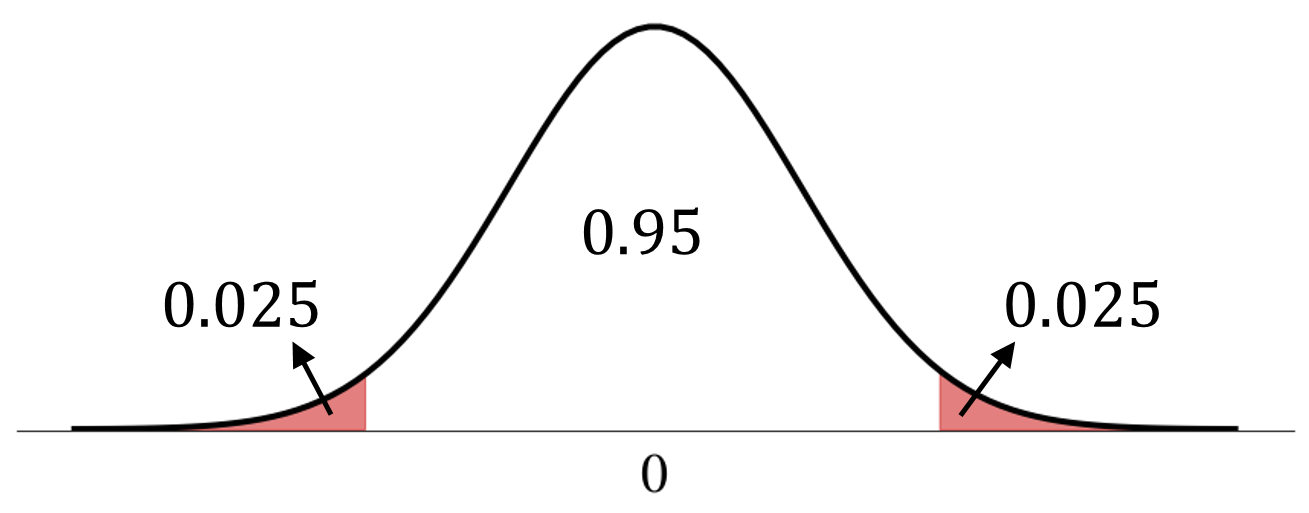

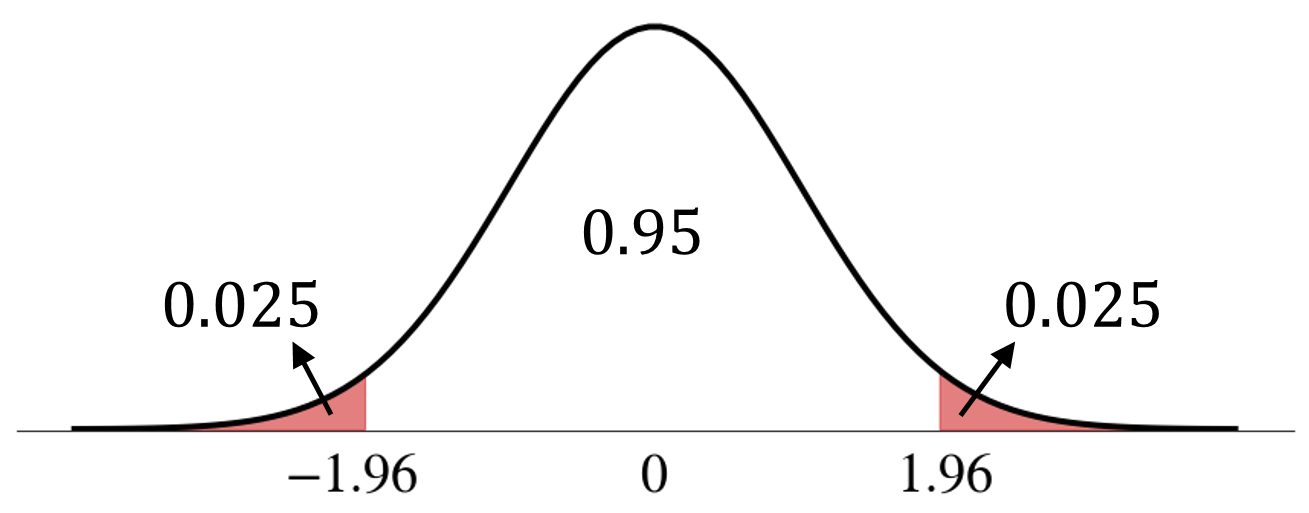

We want

\[

\text{P}\bigg(-1.96 < \frac{\hat{\Theta}_n-\theta}{\sigma/\sqrt{n}} < 1.96\bigg) = 0.95

\]

Multiply through by \(\sigma/\sqrt{n}\)

\[

\small{

\text{P}\bigg(-1.96 \cdot \frac{\sigma}{\sqrt{n}} < \hat{\Theta}_n-\theta < 1.96 \cdot \frac{\sigma}{\sqrt{n}}\bigg) = 0.95

}

\]

Subtract \(\hat{\Theta}_n\) from each term

\[

\small{

\text{P}\bigg(-\hat{\Theta}_n-1.96 \cdot \frac{\sigma}{\sqrt{n}} < -\theta < -\hat{\Theta}_n + 1.96 \cdot \frac{\sigma}{\sqrt{n}}\bigg) = 0.95

}

\]

Multiply through by \(-1\)

\[

\small{

\text{P}\bigg(\hat{\Theta}_n + 1.96 \cdot \frac{\sigma}{\sqrt{n}} > \theta > \hat{\Theta}_n - 1.96 \cdot \frac{\sigma}{\sqrt{n}}\bigg) = 0.95

}

\]

Rearange the sides.

\[

\text{P}\bigg(\hat{\Theta}_n - 1.96 \cdot \frac{\sigma}{\sqrt{n}} < \theta < \hat{\Theta}_n + 1.96 \cdot \frac{\sigma}{\sqrt{n}}\bigg) = 0.95

\]

This means that

\[

\bigg[\hat{\Theta}_n - 1.96 \cdot \frac{\sigma}{\sqrt{n}},\;\; \hat{\Theta}_n + 1.96 \cdot \frac{\sigma}{\sqrt{n}}\bigg]

\]

is a 95% confidence interval.

More compactly, it can be written as \(\hat{\Theta}_n \pm 1.96 \cdot \frac{\sigma}{\sqrt{n}}\)

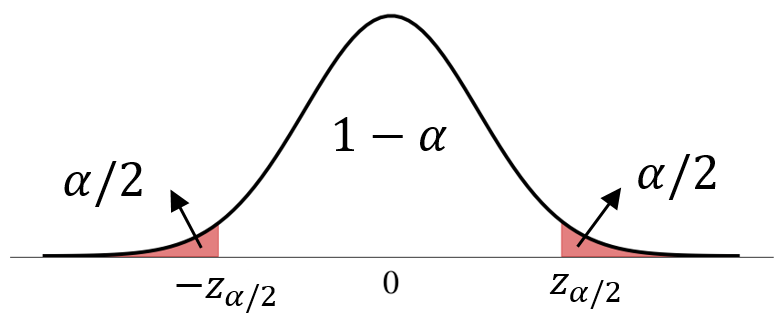

More generally, for a confidence level of \(1-\alpha\),

let \(z_{\frac{\alpha}{2}}\) be such that \(\Phi(z_{\frac{\alpha}{2}})=1-\frac{\alpha}{2}\).

![]()

\[

\small{

\text{P}\bigg(\hat{\Theta}_n - z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}} < \theta < \hat{\Theta}_n + z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}\bigg) = 1-\alpha

}

\]

\[

\small{

\bigg[\hat{\Theta}_n - z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}},\;\; \hat{\Theta}_n + z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}\bigg]}, \;\;\text{or }\;\; \hat{\Theta}_n \pm z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}

}

\]

is a \((1-\alpha)\) confidence interval.

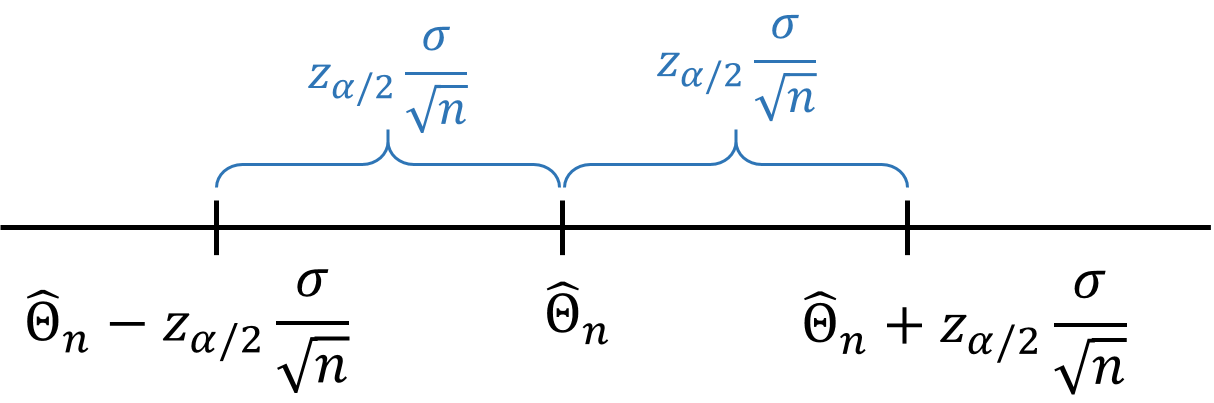

- It is a random interval centered at point estimate \(\hat{\Theta}_n\).

- The half-width of the CI is \(z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}\).

- The width of the CI indicates how precise the estimate is.

\[

\hat{\Theta}_n \pm z_{\alpha/2} \frac{\sigma}{\sqrt{n}}

\]

\[

\text{90% CI: }\;\;\;\; \hat{\Theta}_n \pm 1.645 \frac{\sigma}{\sqrt{n}}

\]

\[

\text{95% CI: }\;\;\;\; \hat{\Theta}_n \pm 1.96 \frac{\sigma}{\sqrt{n}}

\]

\[

\text{99% CI: }\;\;\;\; \hat{\Theta}_n \pm 2.58 \frac{\sigma}{\sqrt{n}}

\]

\[

\hat{\Theta}_n \pm z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}

\]

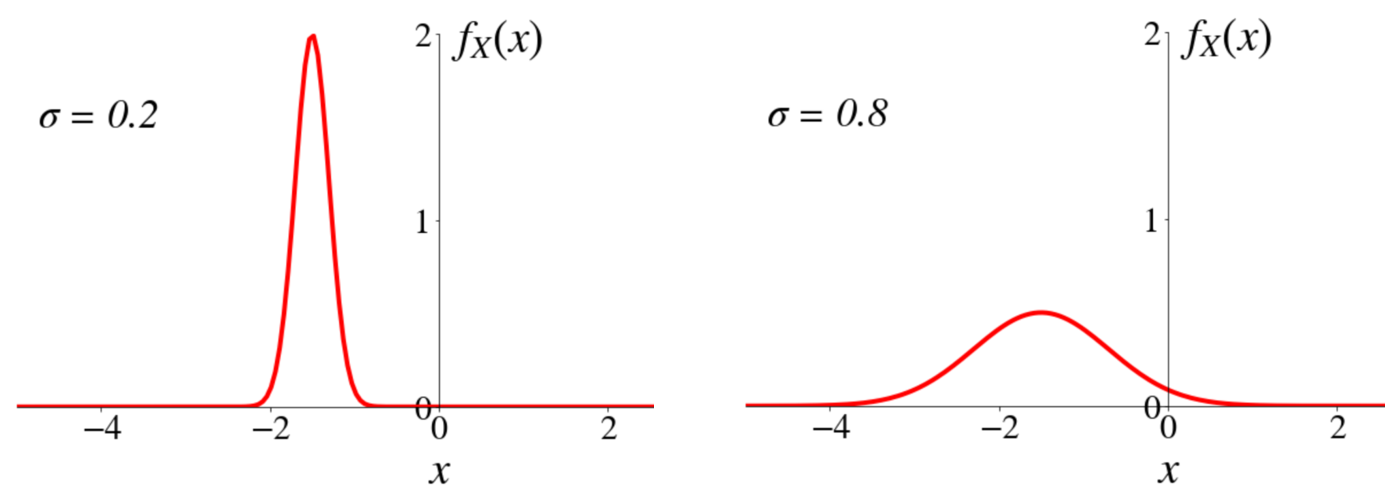

The half-width is proportional to \(\sigma\) (population standard deviation), the inherent variability of the thing we are trying to measure.

\[

\hat{\Theta}_n \pm z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}

\]

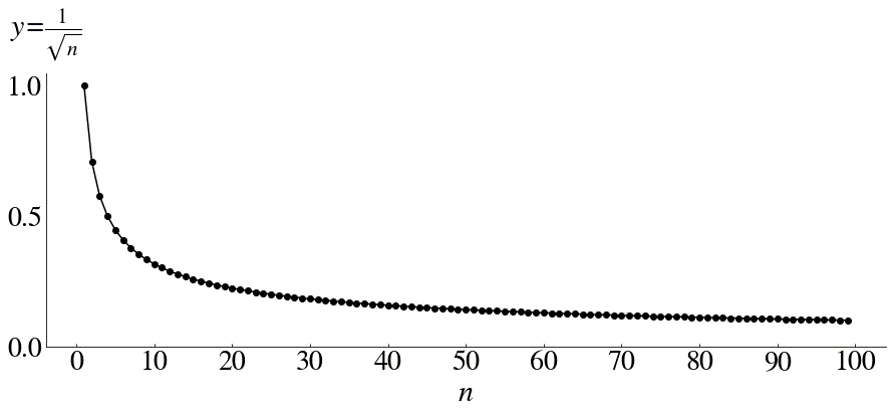

The half-width decreases as sample size \(n\) increases.

Sample size calculation

- We often have a desired precision (i.e., \(\pm 0.5\) hours) and a confidence level (e.g., 99%) for a confidence interval.

- Question: how many data points should we collect?

\[

\text{Half width:}\;\;d=z_{\frac{\alpha}{2}} \cdot \frac{\sigma}{\sqrt{n}}, \;\;\;\;\text{Solve for $n$.}

\]

The sample size needed for a desired half-width of \(d\) is

\[

n=\bigg(z_{\frac{\alpha}{2}} \cdot \frac{\sigma}{d}\bigg)^2

\]

Suppose \(X_1, X_2, \cdots, X_n\) are i.i.d. normal, with unknown mean \(\theta\) and known variance \(\sigma^2\).

\[

\small{

\text{Sample mean estimator:}\;\;\hat{\Theta}_n=\frac{X_1+X_2+\cdots+X_n}{n}

}

\]

\[

\small{

\text{var}\big(\hat{\Theta}_n\big)=\frac{\sigma^2}{n}, \;\;\;\;\sqrt{\text{var}\big(\hat{\Theta}_n\big)}=\frac{\sigma}{\sqrt{n}}

}

\]

The standard deviation of \(\hat{\Theta}_n\) is termed standard error.

\[

\hat{\Theta}_n \pm z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}

\]

The CI above can be expressed in words as

\[

\text{(point estimate)} \pm \text{($z$ critical value}) \cdot \text{(standard error)}

\]

Suppose \(X_1, X_2, \cdots, X_n\) are

- i.i.d. (not necessarily follow a normal distribution)

- with unknown mean \(\theta\) and known variance \(\sigma^2\)

\[

\small{\text{Sample mean estimator:}\;\;\hat{\Theta}_n=\frac{X_1+X_2+\cdots+X_n}{n}}

\]

If \(n\) is sufficiently large, what does the CLT tell us?

\[

\small{

\begin{aligned}

\hat{\Theta}_n \;&\text{ is approximately } \text{N}\bigg(\theta, \frac{\sigma^2}{n}\bigg) \\

\frac{\hat{\Theta}_n-\theta}{\sigma/\sqrt{n}} \;&\text{ is approximately } \text{N}(0, 1) \\

\end{aligned}

}

\]

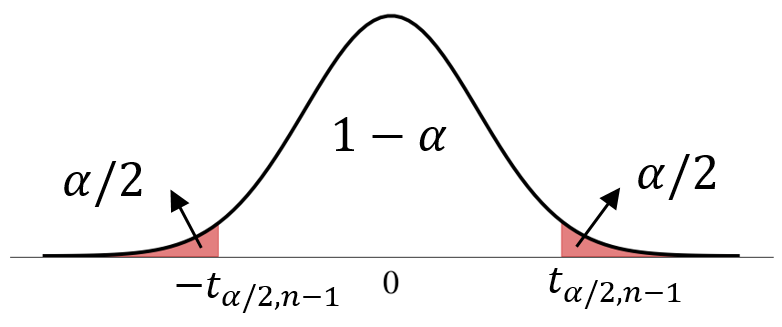

Procedures for constructing a CI

We can proceed exactly as in the previous case.

![]()

\[

\text{P}\bigg(-z_{\frac{\alpha}{2}} < \frac{\hat{\Theta}_n-\theta}{\sigma/\sqrt{n}} < z_{\frac{\alpha}{2}}\bigg) \approx 1-\alpha \;\;\;\color{gray}{\rightarrow \text{by CLT}}

\]

\[

\text{P}\bigg(\hat{\Theta}_n - z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}} < \theta < \hat{\Theta}_n + z_{\frac{\alpha}{2}} \frac{\sigma}{\sqrt{n}}\bigg) \approx 1-\alpha

\]

What if we don’t know \(\sigma^2\)?

Suppose \(X_1, X_2, \cdots, X_n\) are i.i.d. with unknown mean \(\theta\) and unknown variance \(\sigma^2\).

\[

\small{

\text{Sample mean estimator:}\;\;\hat{\Theta}_n=\frac{X_1+X_2+\cdots+X_n}{n}

}

\]

We can estimate the population variance \(\sigma^2\) with

\[

\small{

\text{Sample variance estimator:}\;\;\hat{S}_n^2=\frac{\sum\big(X_i - \hat{\Theta}_n\big)^2}{n-1}

}

\]

\[

\small{

\frac{\hat{\Theta}_n-\theta}{\sigma/\sqrt{n}} \sim \text{N}(0, 1), \; \text{if $X_i$ is normally distributed.}

}

\]

\[

\small{

\frac{\hat{\Theta}_n-\theta}{\sigma/\sqrt{n}} \text{ is approximately } \text{N}(0, 1), \; \text{if $X_i$ is not normal, but $n$ is large.}

}

\]

Once we replace \(\sigma\) with \(\hat{S}_n\), we have

\[

\small{

\frac{\hat{\Theta}_n-\theta}{\hat{S}_n/\sqrt{n}}

}

\]

\[

\small{

\frac{\hat{\Theta}_n-\theta}{\hat{S}_n/\sqrt{n}} \text{ is approximately } \text{N}(0, 1), \; \text{if $n$ is sufficiently large.}

}

\]

If \(n\) is sufficiently large,

\[

\small{

\text{P}\bigg(-z_{\frac{\alpha}{2}} < \frac{\hat{\Theta}_n-\theta}{\hat{S}_n/\sqrt{n}} < z_{\frac{\alpha}{2}}\bigg) \approx 1-\alpha

}

\]

Generally speaking, \(n>40\) would be sufficient.

\[

\small{

\hat{\Theta}_n \pm z_{\frac{\alpha}{2}} \frac{\hat{S}_n}{\sqrt{n}}

}

\]

is a CI for \(\theta\) with confidence level approximately \(1-\alpha\).

\[

\small{

\text{(point estimate)} \pm \text{($z$ critical value)} \cdot \text{(estimated standard error)}

}

\]

What if the sample size \(n\) is small?

Suppose \(X_1, X_2, \cdots, X_n\) are i.i.d. normal with unknown mean \(\theta\) and unknown variance \(\sigma^2\).

\[

\small{

\text{Sample mean estimator:}\;\;\hat{\Theta}_n=\frac{X_1+X_2+\cdots+X_n}{n}

}

\]

\[

\small{

T_n=\frac{\hat{\Theta}_n-\theta}{\hat{S}_n/\sqrt{n}}

}

\]

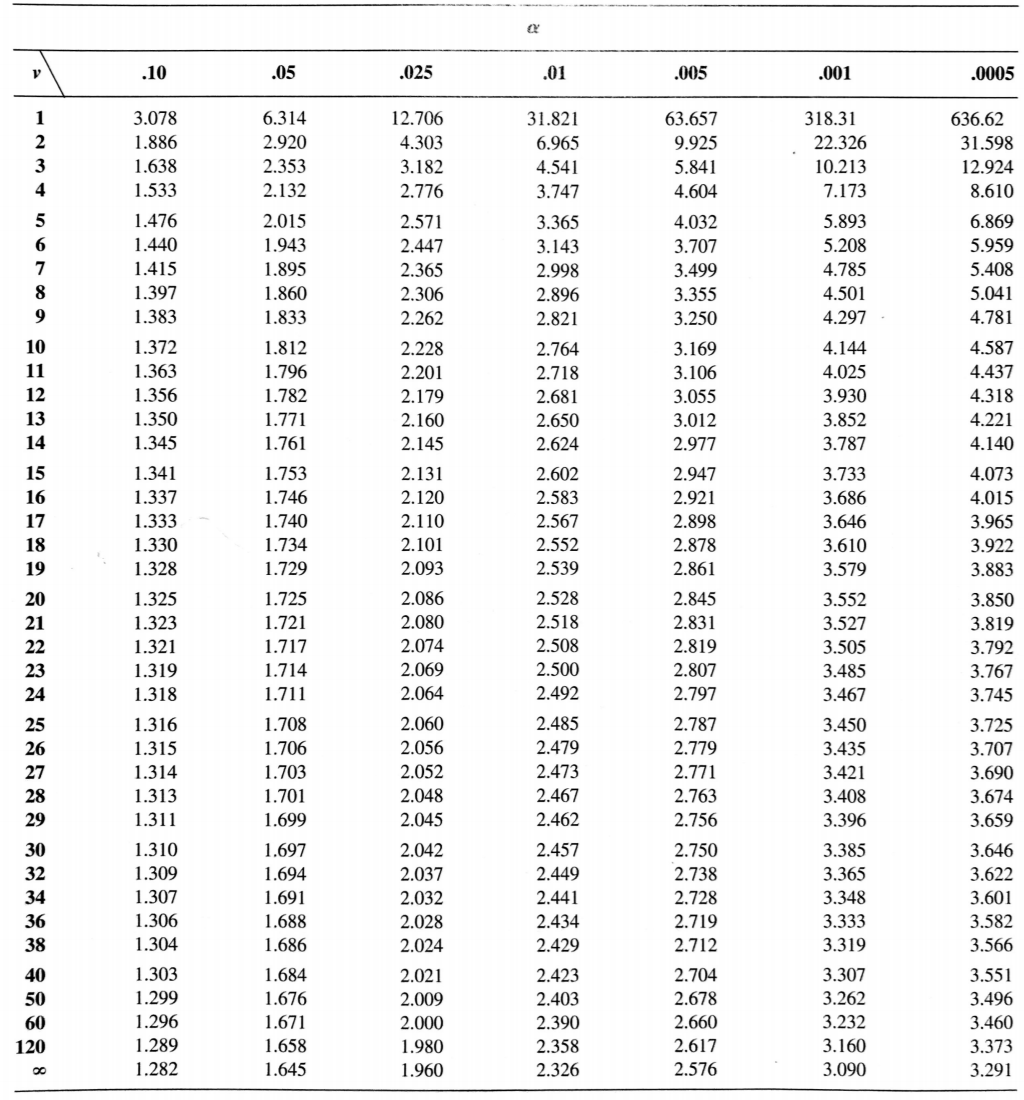

has a probability distribution called a t-distribution with \(v=n-1\) degrees of freedom.

\[

\small{

t\text{-distribution:}\;\;\;T_n=\frac{\hat{\Theta}_n-\theta}{\hat{S}_n/\sqrt{n}}

}

\]

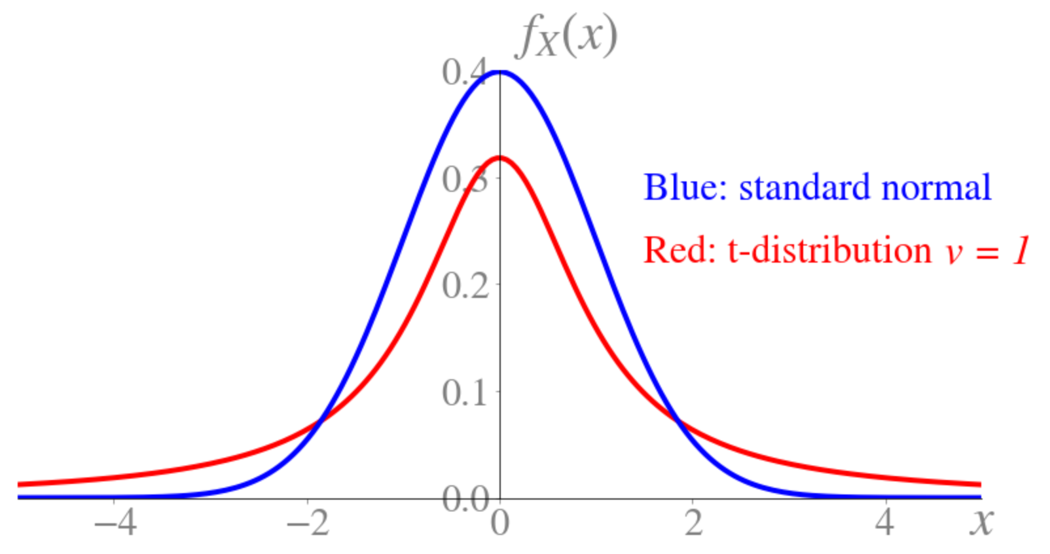

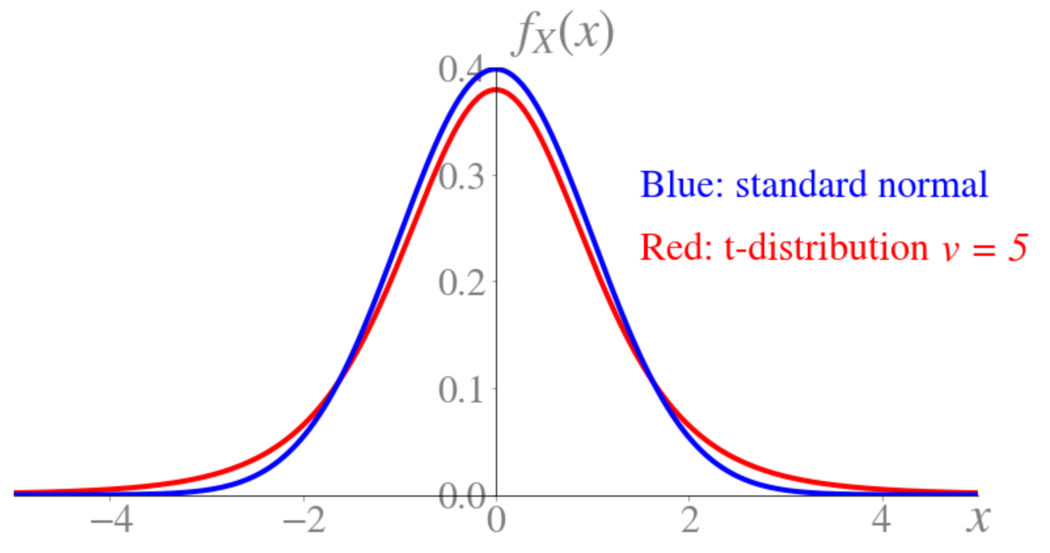

t-distribution

- Symmetric

- Bell-shaped

- More spread out than \(N(0, 1)\)

- Approaches \(N(0, 1)\) as \(v\rightarrow +\infty\)