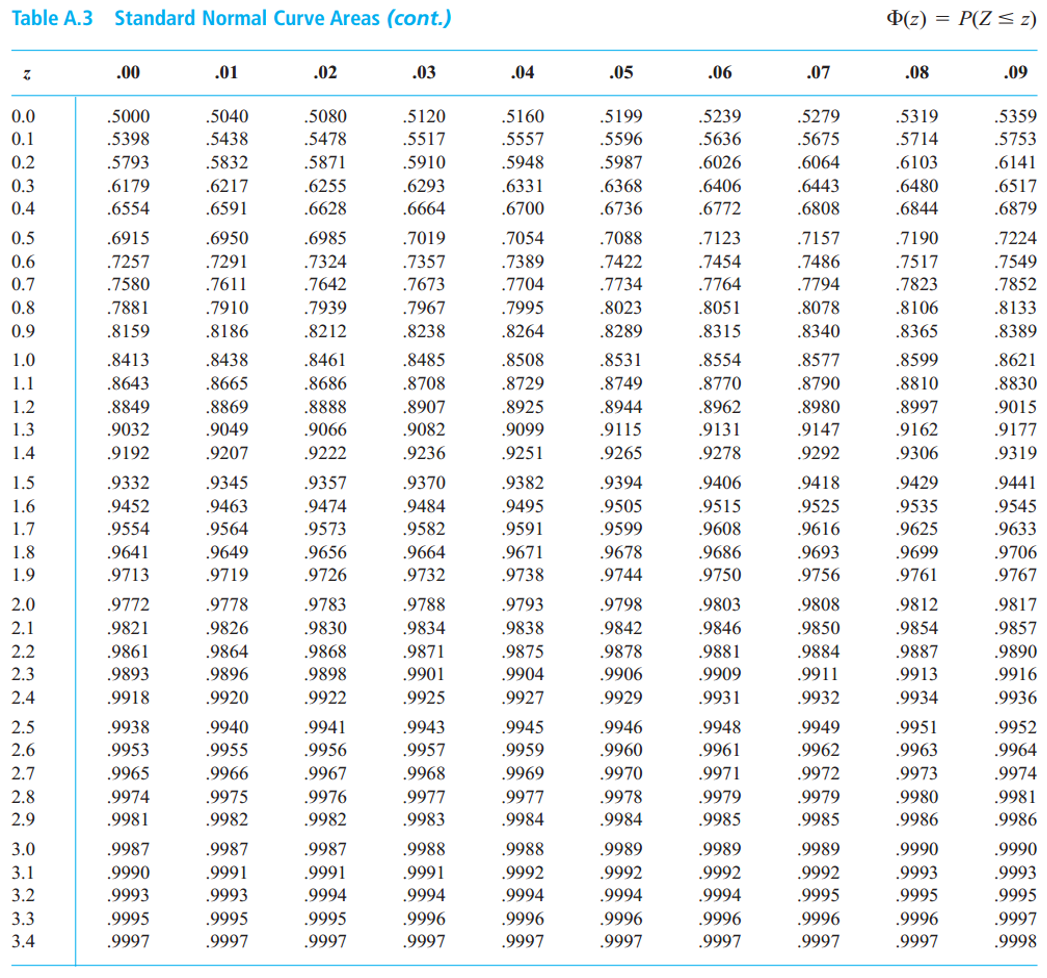

6.3 Central limit theorem

Let \(X_1, X_2, \cdots, X_n\) be i.i.d. with \(\mu\) and \(\sigma^2\).

\[

\small{

\begin{aligned}

\bar{X}_n&=\frac{X_1+X_2+\cdots+X_n}{n} \\

\\

S_n&=X_1+X_2+\cdots+X_n \\

\end{aligned}

}

\]

Then, if \(n\) is large,

\[

\begin{aligned}

&\bar{X}_n \text{ is approximately } \text{N}(\mu, \frac{\sigma^2}{n}) \\

&S_n \text{ is approximately } \text{N}(n\mu, n\sigma^2) \\

\end{aligned}

\]

\[

\begin{aligned}

&\bar{X}_n \text{ is approximately } \text{N}(\mu, \frac{\sigma^2}{n}) \\

&S_n \text{ is approximately } \text{N}(n\mu, n\sigma^2) \\

\end{aligned}

\]

Their standardized version: \[

\begin{aligned}

\frac{\bar{X}_n-\mu}{\sigma/\sqrt{n}} &\text{ is approximately } \text{N}(0, 1) \\

\\

\frac{S_n-n\mu}{\sqrt{n}\sigma} &\text{ is approximately } \text{N}(0, 1) \\

\end{aligned}

\]

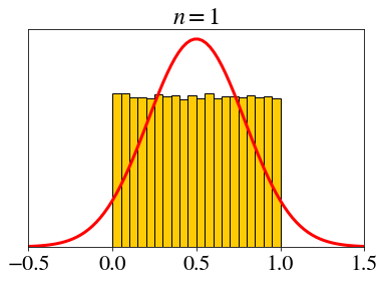

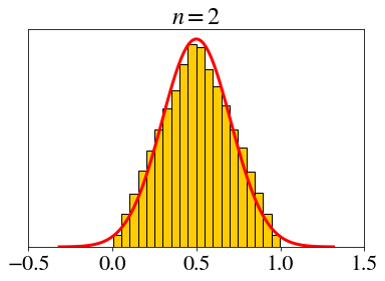

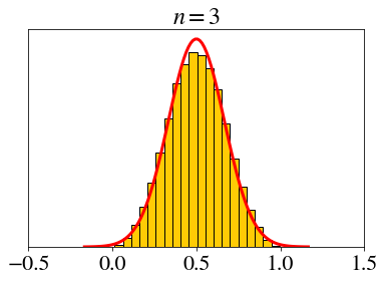

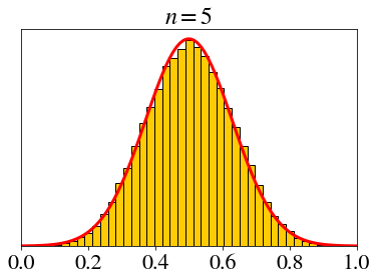

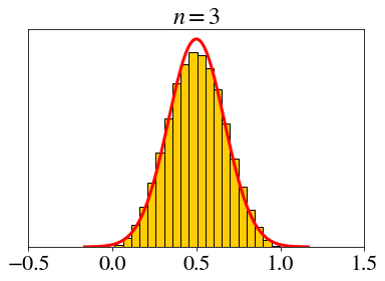

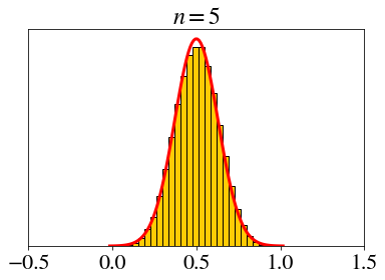

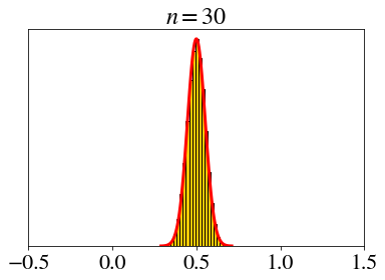

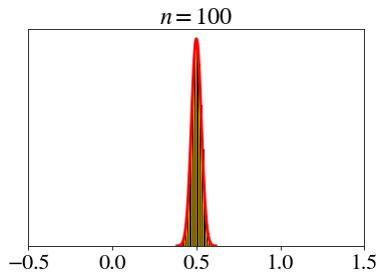

\[

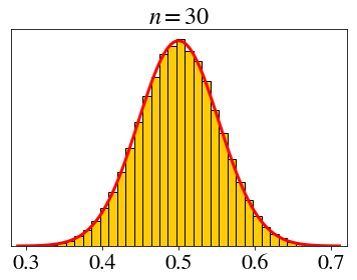

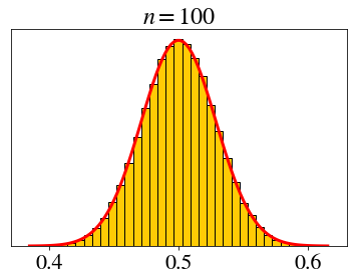

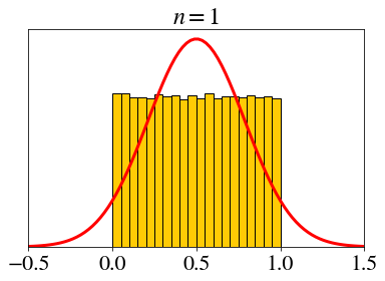

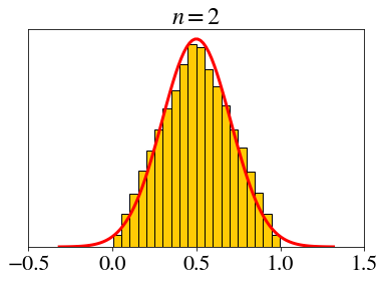

X_i \sim \text{unif}(0, 1),\;\; \bar{X}_n=\frac{X_1+X_2+\cdots+X_n}{n}

\]

\[

X_i \sim \text{unif}(0, 1),\;\; \bar{X}_n=\frac{X_1+X_2+\cdots+X_n}{n}

\]

Let’s set a fixed x-axis scale.

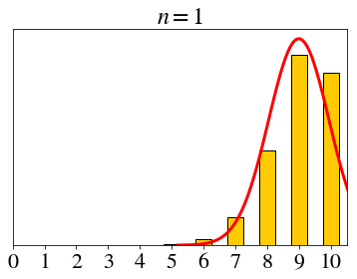

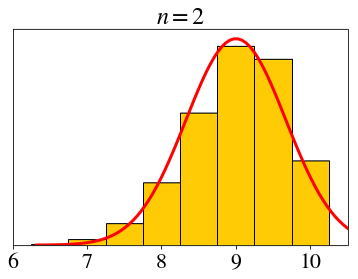

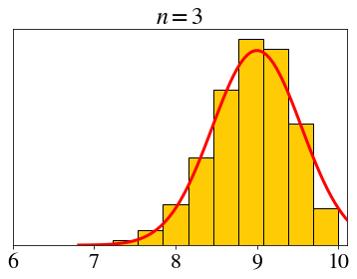

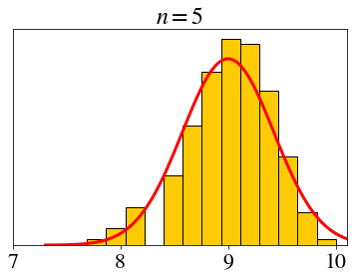

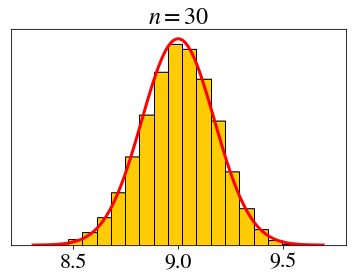

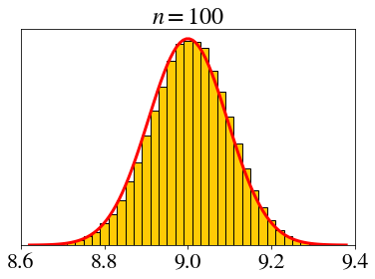

\[

X_i \sim \text{bin}(10, 0.9),\;\; \bar{X}_n=\frac{X_1+X_2+\cdots+X_n}{n}

\]

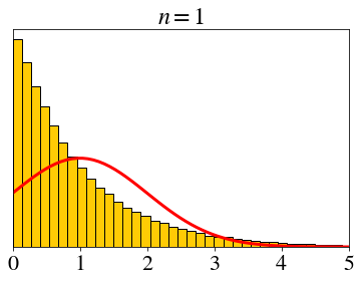

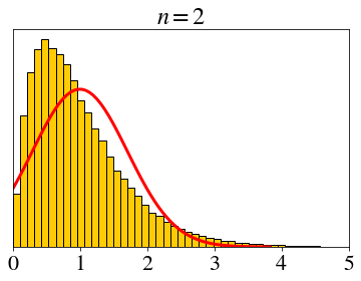

\[

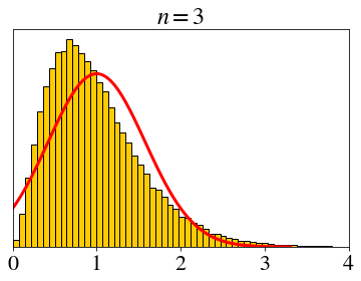

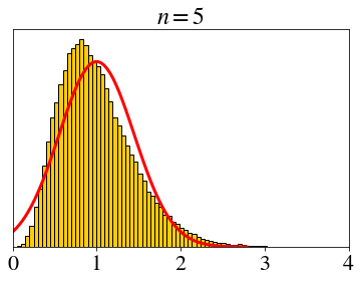

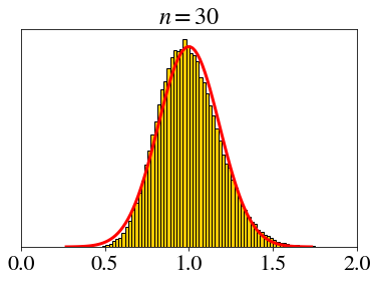

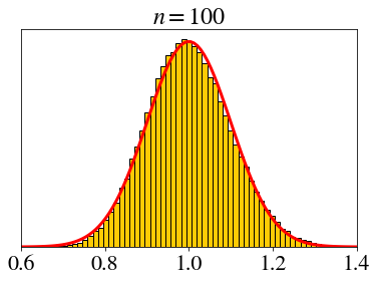

X_i \sim \text{expo}(1),\;\; \bar{X}_n=\frac{X_1+X_2+\cdots+X_n}{n}

\]

How big does \(n\) need to be for the CLT?

- Not very big.

- Rule of thumb: \(n > 30\)

\[

\text{bin}(10, 0.9)

\]

Exercise

- An accountant rounds each transaction to the nearest dollar (e.g., from $8.63 to $9).

- Assume the error in rounding is \(\text{unif}(-0.5, 0.5)\).

- There is a total of 300 transaction entries today.

- What is the probability that the total error in today’s transactions is more than $5?