Normal distribution

A continuous RV \(X\) is normal if it has a PDF:

\[

f_X(x)=\frac{1}{\sigma\sqrt{2\pi}}e^{-\frac{1}{2}(\frac{x-\mu}{\sigma})^2}

\]

\[

\text{where } \mu \text{ and } \sigma \text{ are its two parameters } (\sigma >0).

\]

\[

X \sim \text{N}(\mu, \sigma^2)

\]

Normal distribution

\[

\begin{aligned}

X &\sim \text{N}(\mu, \sigma^2) \\

\\

f_X(x)&=\frac{1}{\sigma\sqrt{2\pi}}e^{-\frac{1}{2}(\frac{x-\mu}{\sigma})^2} \\

\\

\text{E}[X]&=\mu \\

\\

\text{var}(X)&=\sigma^2 \\

\end{aligned}

\]

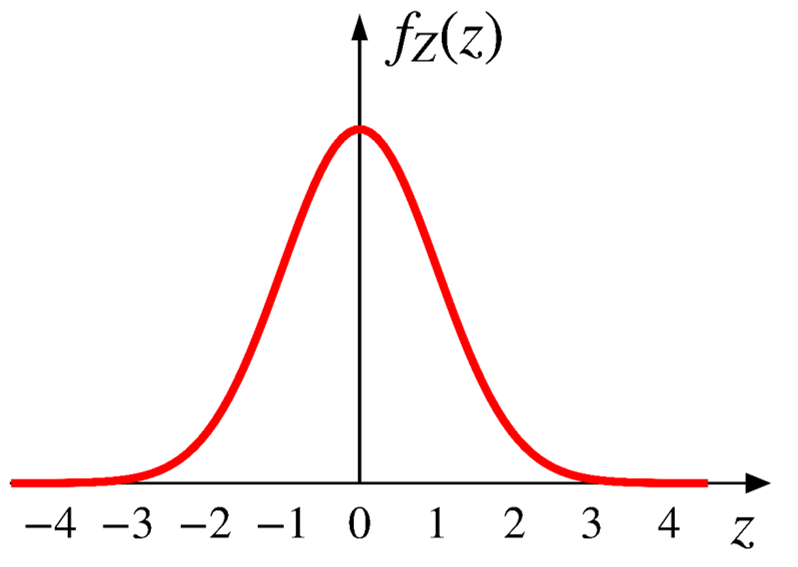

First, we show that the expected value of a standard normal RV \(Z \sim \text{N}(0, 1)\) is zero.

\[

\begin{aligned}

f_Z(z)&=\frac{1}{\sqrt{2\pi}}e^{-\frac{z^2}{2}} \\

\\

\text{E}[Z]&=\int_{-\infty}^{+\infty}z(\frac{1}{\sqrt{2\pi}}e^{-\frac{z^2}{2}})dz=0 \\

\end{aligned}

\]

The integration above is 0 as for any odd function \(g(x)\) (i.e., \(g(-x)=-g(x)\) ), we have \(\int_{-a}^a g(x)dx=0\) .

Let

\[Z=\frac{X-\mu}{\sigma} \;\;\;\;(\text{or } X=\sigma Z+\mu)\]

We have

\[f_X(x)=\frac{1}{\sigma\sqrt{2\pi}}e^{-\frac{1}{2}(\frac{x-\mu}{\sigma})^2}\]

\[X \sim \text{N}(\mu, \sigma^2)\]

\[\text{E}[X]=\text{E}[\sigma Z+\mu]=\sigma\text{E}[Z]+\mu=\sigma\cdot 0+\mu=\mu\]

We can also prove for \(Z \sim \text{N}(0, 1)\) , \(\text{var}(Z)=1\) .

\[

\begin{aligned}

\text{var}(Z)&=\text{E}\big[Z^2\big]-\big(\text{E}[Z]\big)^2 \\

\\

&=\int_{-\infty}^{+\infty}z^2(\frac{1}{\sqrt{2\pi}}e^{-\frac{z^2}{2}})dz \\

\\

&=1 \;\;\;\;\color{gray}{\rightarrow\text{we will skip the proof of this part.}}

\end{aligned}

\]

Then we have \[\text{var}(X)=\text{var}(\sigma Z+\mu)=\sigma^2\text{var}(Z)=\sigma^2 \cdot 1 = \sigma^2\]

Properties

Normality is preserved by linear transformations.

If

\[

X \sim \text{N}(\mu, \sigma^2)

\]

and

\[

Y=aX+b, \;\; \text{for any constants } a \;(\neq0) \text{ and $b$.}

\]

we have

\[

Y \sim \text{N}(a\mu+b, a^2\sigma^2)

\]

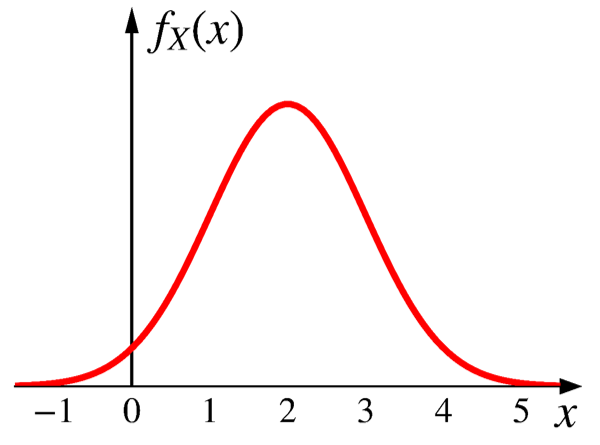

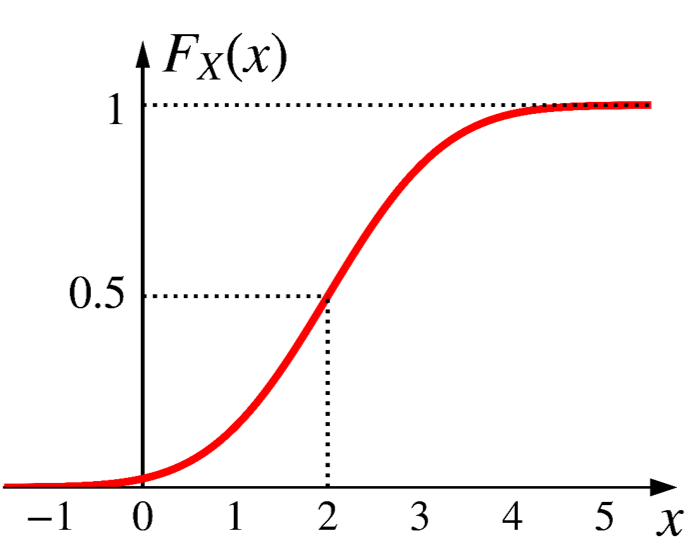

CDF of normal distribution

\[

X \sim \text{N}(2, 1)

\]

CDF of normal distribution

\[

\begin{aligned}

F_X(x)&=\text{P}(X \leq x) \\

\\

&=\int_{-\infty}^x \frac{1}{\sigma\sqrt{2\pi}}e^{-\frac{1}{2}\big(\frac{t-\mu}{\sigma}\big)^2}dt \\

\\

&=\frac{1}{\sigma\sqrt{2\pi}}\int_{-\infty}^x e^{-\frac{1}{2}\big(\frac{t-\mu}{\sigma}\big)^2}dt \\

\end{aligned}

\]

Unfortunately, there is no closed-form expression for the integration above.

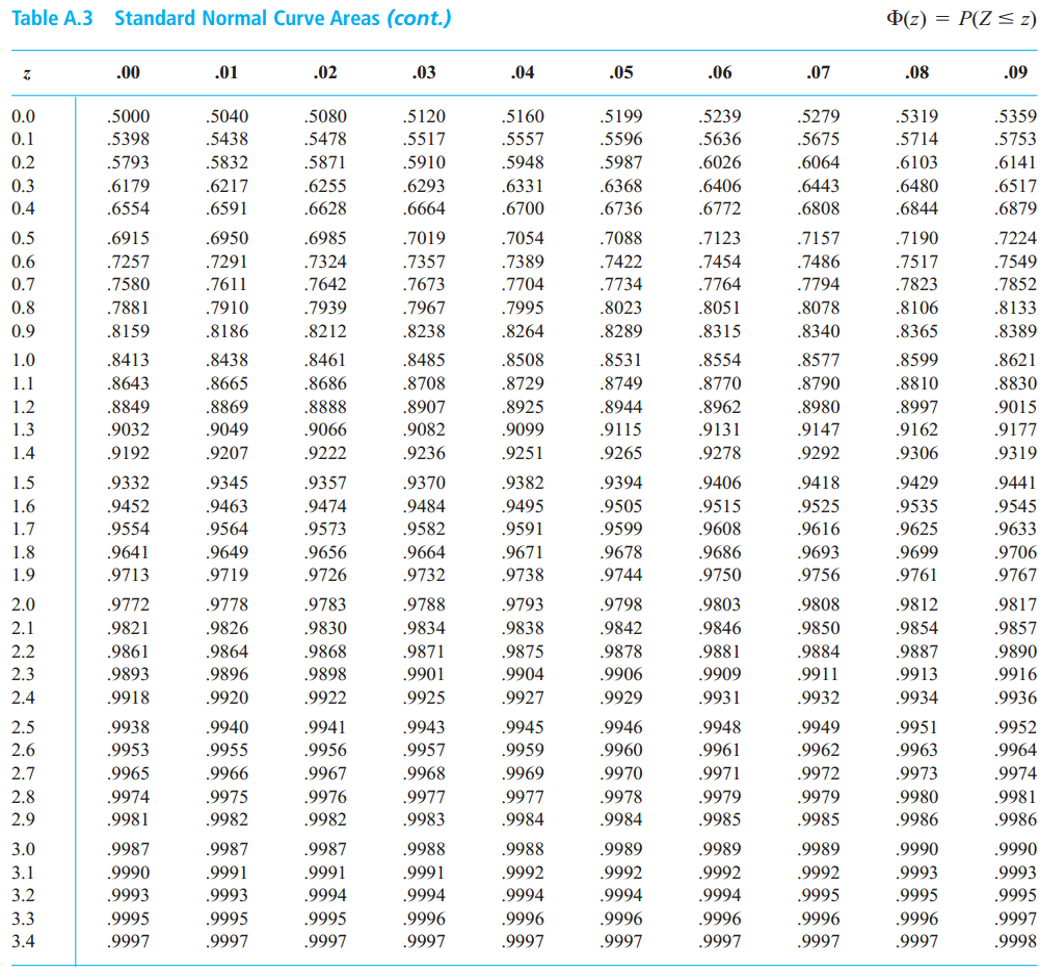

CDF of standard normal distribution

\[

F_Z(z)=\Phi(z)=\text{P}(Z \leq z)=\frac{1}{\sqrt{2\pi}}\int_{-\infty}^z e^{-\frac{t^2}{2}}dt

\]

Standard normal table (or Z table)

The table only contains values of \(\Phi(z)\) for \(z \geq 0\) .

What if \(z < 0\) ?

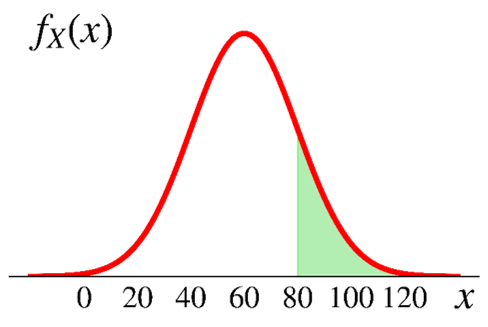

Exercise

Assume the annual snowfall in Dearborn follows a normal distribution with

a mean of 60 inches

a standard deviation of 20 inches

What is the probability this year has 80+ inches snow?

\[

X \sim \text{N}\big(\mu, \sigma^2\big)

\]

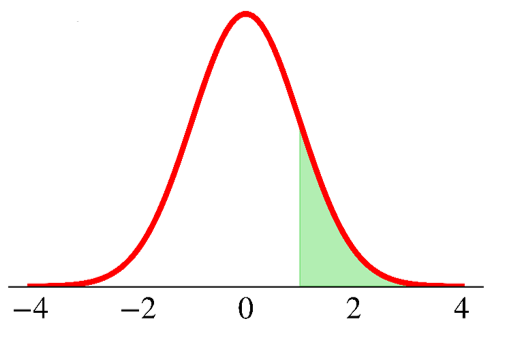

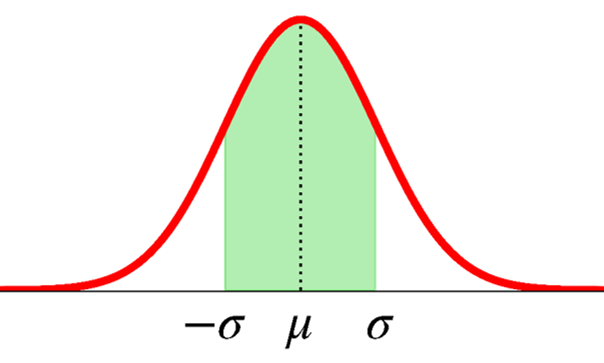

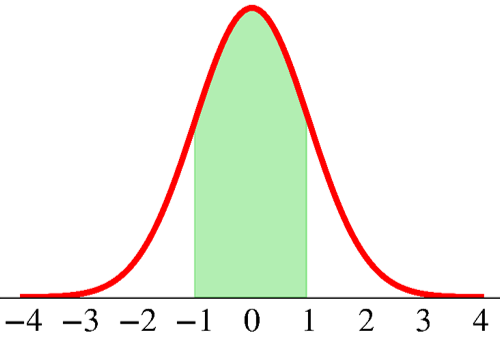

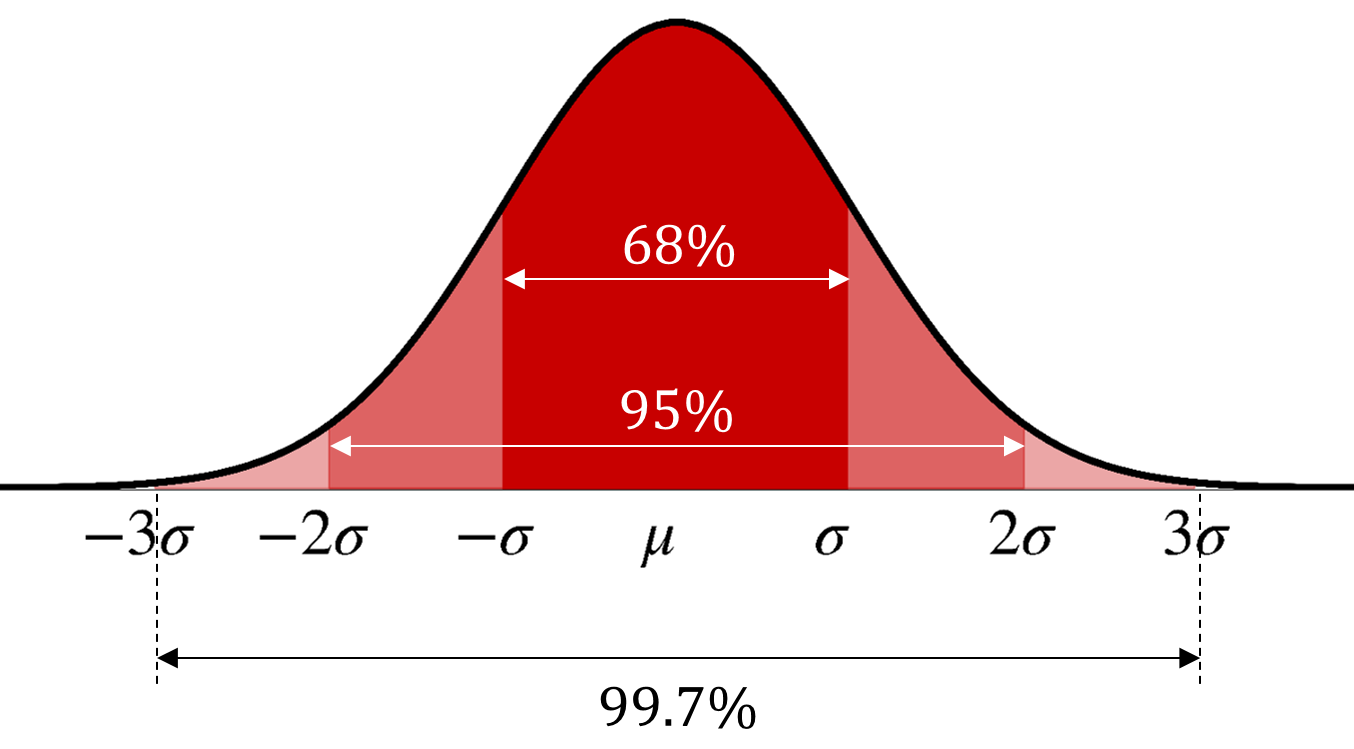

What is the probability that \(X\) takes values within one standard deviation from its mean?

\[

\text{P}(\mu - \sigma < X < \mu + \sigma) = \;?

\]

\[

X \sim \text{N}\big(\mu, \sigma^2\big)

\]

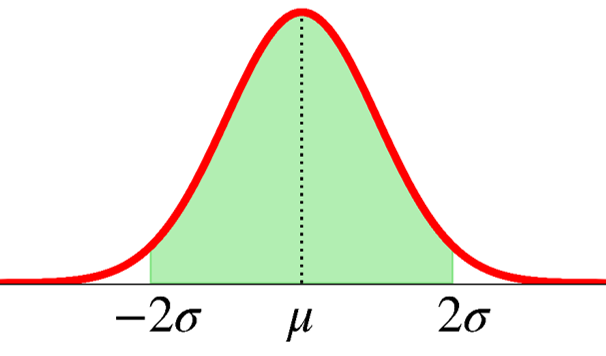

What is the probability that \(X\) takes values within two standard deviation from its mean?

\[

\text{P}(\mu - 2\sigma < X < \mu + 2\sigma) = \;?

\]

\[

X \sim \text{N}\big(\mu, \sigma^2\big)

\]

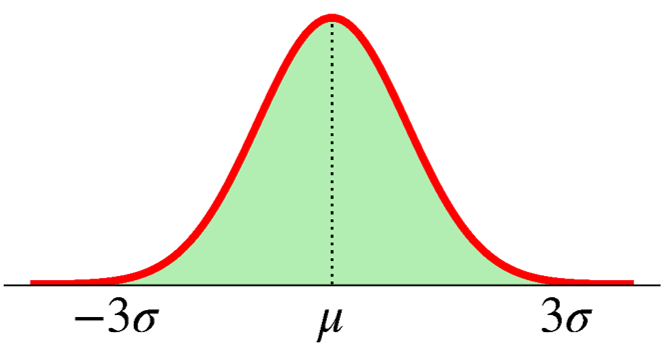

What is the probability that \(X\) takes values within three standard deviation from its mean?

\[

\text{P}(-3\sigma < X < 3\sigma) = \;?

\]

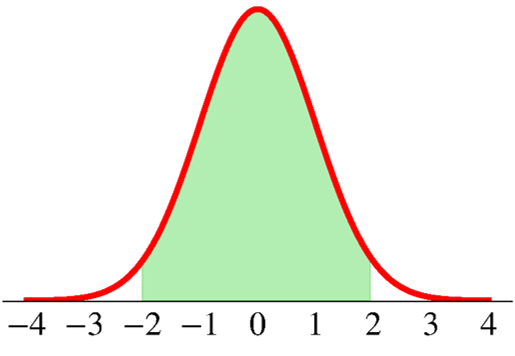

68-95-99.7 rule

\[

X \sim \text{N}\big(\mu, \sigma^2\big)

\]

Six Sigma

\[

\text{P}(\mu - 6\sigma < X < \mu + 6 \sigma)=99.99966\%

\]

The procedure to get the normal CDF

Standardize \(X\) to obtain the standard normal \(Z\) \[\small{Z=\frac{X-\mu}{\sigma}}\]

Obtain the CDF value from the \(Z\) table

\[

\small{

\begin{aligned}

\text{P}(X < x)&=\text{P}\bigg(\frac{X-\mu}{\sigma} < \frac{x-\mu}{\sigma}\bigg)\\

&=\text{P}\bigg(Z < \frac{x-\mu}{\sigma}\bigg)

=\Phi\bigg(\frac{x-\mu}{\sigma}\bigg) \\

\end{aligned}

}

\]

Getting normal CDF in Python

Go to Google Colab and sign in. Open a new notebook.

# get the CDF of a standard normal distribution from scipy import stats= 0 )

How about \(F_X(x=0)=\text{P}(X \leq 0)\) where \(X \sim \text{N}(1, 3^2)\) ?

# get the CDF of a non-standard normal distribution = 0 , loc= 1 , scale= 3 )

Mixed random variables

As a final note to Chapter 3 & 4, a random variable could be a mixture of both discrete & continuous.

Consider the following game of tossing a coin

If it lands on heads, you get $10.

If it lands on tails, you get $ amount of \(\text{unif}(5, 15)\) .